The IPPF: Global internal audit standards, requirements, and guidance

The International Professional Practices Framework® (IPPF®) provides internal audit standards, requirements, and guidance that offer a structural blueprint and coherent system to facilitate consistent development, interpretation, and application of knowledge for the internal audit profession.

International Professional Practices Framework (IPPF) for internal auditing

The International Professional Practices Framework (IPPF) organizes the authoritative body of knowledge on internal auditing, promulgated by The Institute of Internal Auditors.

State of the Standards Survey

Share your thoughts in The IIA's global State of the Standards survey, open from June 1 to June 30. Your input, based on real-world experiences, will help inform future Topical Requirements and Global Guidance, companion resources, advocacy priorities, and updates to the IPPF and Global Standards. The survey takes about 15 minutes to complete, is available in multiple languages, and is open to all interested parties—internal auditors, stakeholders, members, and nonmembers worldwide.

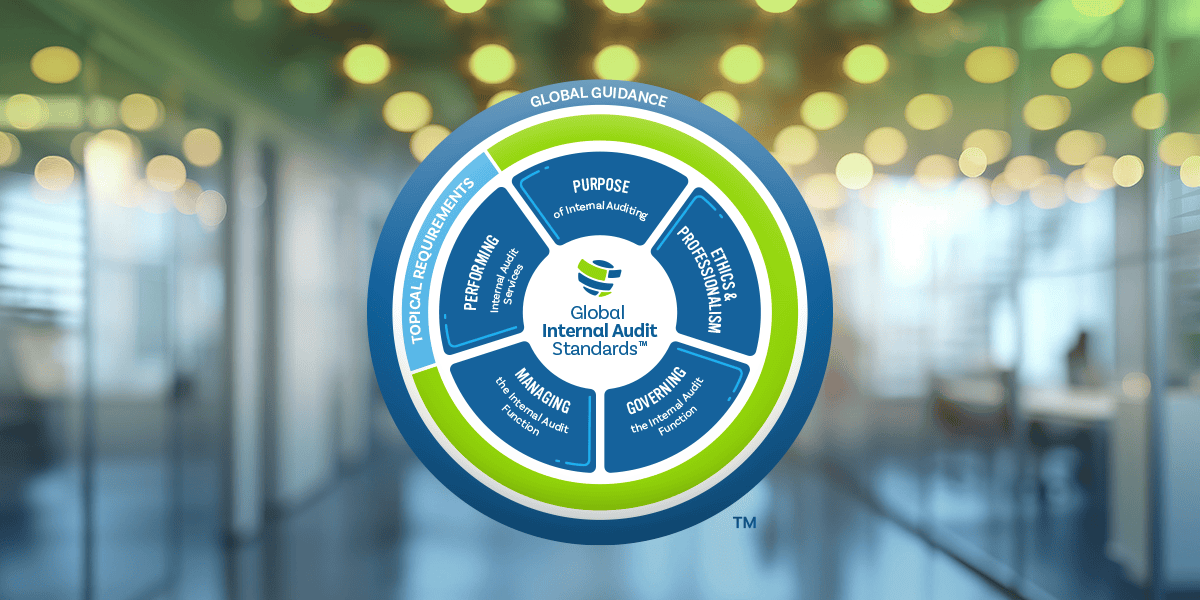

What comprises the IPPF standards and guidance?

The IPPF consists of the Global Internal Audit Standards™, Topical Requirements, and Global Guidance.

What is the purpose of internal auditing?

Domain I: Purpose of Internal Auditing

Internal auditing strengthens the organization’s ability to create, protect, and sustain value by providing the board and management with independent, risk-based, and objective assurance, advice, insight, and foresight.

How does internal auditing enhance the organization?

Internal auditing enhances the organization’s:

- Successful achievement of its objectives.

- Governance, risk management, and control processes.

- Decision-making and oversight.

- Reputation and credibility with its stakeholders.

- Ability to serve the public interest.

When is internal auditing is most effective?

Internal auditing is most effective when:

- It is performed by competent professionals in conformance with the Global Internal Audit Standards, which are set in the public interest.

- The internal audit function is independently positioned with direct accountability to the board.

- Internal auditors are free from undue influence and committed to making objective assessments.

Why are internal auditing standards important?

The IIA’s Global Internal Audit Standards guide the worldwide professional practice of internal auditing and serve as a basis for evaluating and elevating the quality of the internal audit function. They set forth principles, requirements, considerations, and examples for the professional practice of internal auditing globally and help internal auditors and internal audit functions achieve the Purpose of Internal Auditing.

While the primary function of internal auditing is to strengthen governance, risk management, and control processes, its effects extend beyond the organization. Internal auditing contributes to an organization’s overall stability and sustainability by providing assurance on its operational efficiency, reliability of reporting, compliance with laws and/or regulations, safeguarding of assets, and ethical culture. This, in turn, fosters public trust and confidence in the organization and the broader systems of which it is a part. Thus, internal auditing plays a critical role in enhancing an organization’s ability to serve the public interest.

IIA Membership grants exclusive access to internal audit thought leadership, tools, and guidance

Become more effective and efficient when following internal audit industry standards with access to exclusive Global Guidance and IIA Audit Tools on issues affecting internal auditors worldwide.

When was the IPPF updated?

The 2024 IPPF was released on January 9, 2024.

- The Standards Board released the Global Internal Audit Standards, the IPPF's main component, updating the mandatory guidance of the International Professional Practices Framework.

- The 2024 IPPF supersedes (replaces) the 2017 IPPF.

- Internal audit functions were required to adopt the 2024 IPPF Global Internal Audit Standards as of January 9, 2025.

-

2024 IPPF

The 2024 International Professional Practices Framework® (IPPF®) includes Global Internal Audit Standards™, Topical Requirements, and Global Guidance.

IPPF mandatory components

The 2024 Global Internal Audit Standards are a mandatory component of the 2024 IPPF and incorporate all the mandatory elements of the 2017 IPPF, plus the 2017 IPPF’s Implementation Guidance.

The Global Internal Audit Standards incorporate content from the six elements of the 2017 IPPF:

- Mission of Internal Audit

- Definition of Internal Auditing (mandatory)

- Core Principles for the Professional Practice of Internal Auditing (mandatory)

- Code of Ethics (mandatory)

- International Standards for the Professional Practice of Internal Auditing (mandatory)

- Implementation Guidance (recommended) has been incorporated into the 2024 Standards as considerations for implementation and examples of evidence of conformance.

These elements no longer exist as separate entities.

Topical Requirements were added as a mandatory component of the 2024 IPPF and aim to enhance the consistency and quality of internal audit services related to specific risk areas.

IPPF recommended components

Global Guidance continues to be a recommended component in the 2024 IPPF, providing in-depth information about various internal audit practices and subjects.

-

The Standards are effective for quality assessments January 9, 2025.

For information about quality assessments, visit IIA Quality Services.

-

The 2024 edition of the Quality Assessment Manual is available in eBook and hardcover formats for purchase from The IIA Bookstore.

This edition incorporates the requirements of the 2024 Global Internal Audit Standards, effective for quality assessments beginning January 9, 2025.

-

Those who have successfully completed all three Certified Internal Auditor® (CIA®) exam parts and earned the CIA certification will not be required to retest or earn a new credential.

No actions are required other than fulfilling the requirements of the annual certification renewal policy.

-

Details about the most recent processes appear in the Report on the Standard-setting and Public Comment Processes for the Global Internal Audit Standards™.

-

For questions about downloading, copying, reprinting, and distributing the Standards, review the Copyright Notice or email copyright@theiia.org.

-

The Standards have been translated into more than 30 languages.

-

Institutes that wish to translate a specific document should use this request form.

Institutes that have questions about translations can email translation.services@theiia.org.

The IIA is no longer authorizing translation of the 2017 International Standards for the Professional Practice of Internal Auditing. However, existing translations may be accessed for historical reference.

IPPF internal audit standards frequently asked questions

Acknowledgements

"The IIA is grateful to members of the International Internal Audit Standards Board past and present who devoted countless hours of their time as volunteers to this worthy project. The Global Internal Audit Standards are the culmination of years of research, outreach, feedback, and due diligence, all of which were vital to crafting Standards that reflect the vision, breadth, and depth of our profession and the needs of the organizations we serve. The IIASB thanks the IPPF Oversight Council, IIA members and staff, IIA affiliates, internal audit practitioners, and other stakeholders that contributed their time and feedback throughout the process. The perspectives shared were invaluable in shaping the Standards to address the evolving needs and challenges faced by audit professionals and organizations worldwide."

Naohiro Mouri, CIA, CPA, Chairman, International Internal Audit Standards Board

J. Michael Peppers, CIA, QIAL, CRMA, CPA, Immediate Past Chairman, International Internal Audit Standards Board