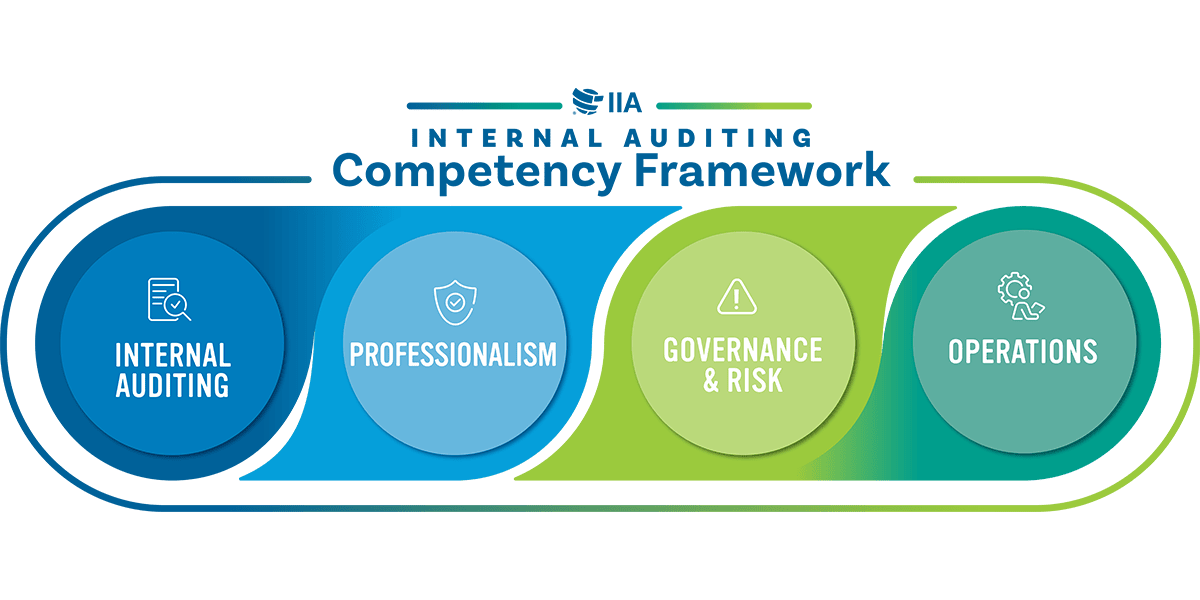

New Internal Auditing Competency Framework

Discover the new Internal Auditing Competency Framework™, designed to optimize knowledge and skills across four key areas and 28 subcategories. The Global Practice Guide and Templates provide a customizable framework that will help internal auditors, chief audit executives, and other audit leaders to define and meet the expectations of their roles and plan for their future success.

Your roadmap to success through professional best practices

Strategically align competencies and tailor proficiency levels and job roles to deliver robust, insightful assurance and advisory services.

Authoritative IIA Global Guidance and Tools

Competencies to meet the future of internal auditing

Continued success hinges on staying current.

Our new Internal Auditing Competency Framework aligns with the Global Internal Audit Standards™ and best practices, empowering auditors to lead confidently and effectively.

Map your way to future success

Flexible and customizable for your priorities

Our new Internal Auditing Competency Framework Global Practice Guide and members-only Templates work together to provide clarity, direction, and actionable guidance, ensuring you have the essential skills to thrive professionally and add lasting value.