Future of the IPPF Evolution

The International Internal Audit Standards Board has completed a major milestone in the IPPF Evolution, a multiyear project to update the mandatory guidance of the International Professional Practices Framework. On January 9, 2024, the Standards Board released the Global Internal Audit Standards™, the IPPF's main component, which will replace the 2017 International Standards for the Professional Practice of Internal Auditing, effective January 9, 2025. The 2017 Standards remain in effect during the 12-month transition period. Internal audit functions are required to adopt the new Global Internal Audit Standards by January 9, 2025.

Access the 2024 Global Internal Audit Standards

Access the 2017 Standards and related materials

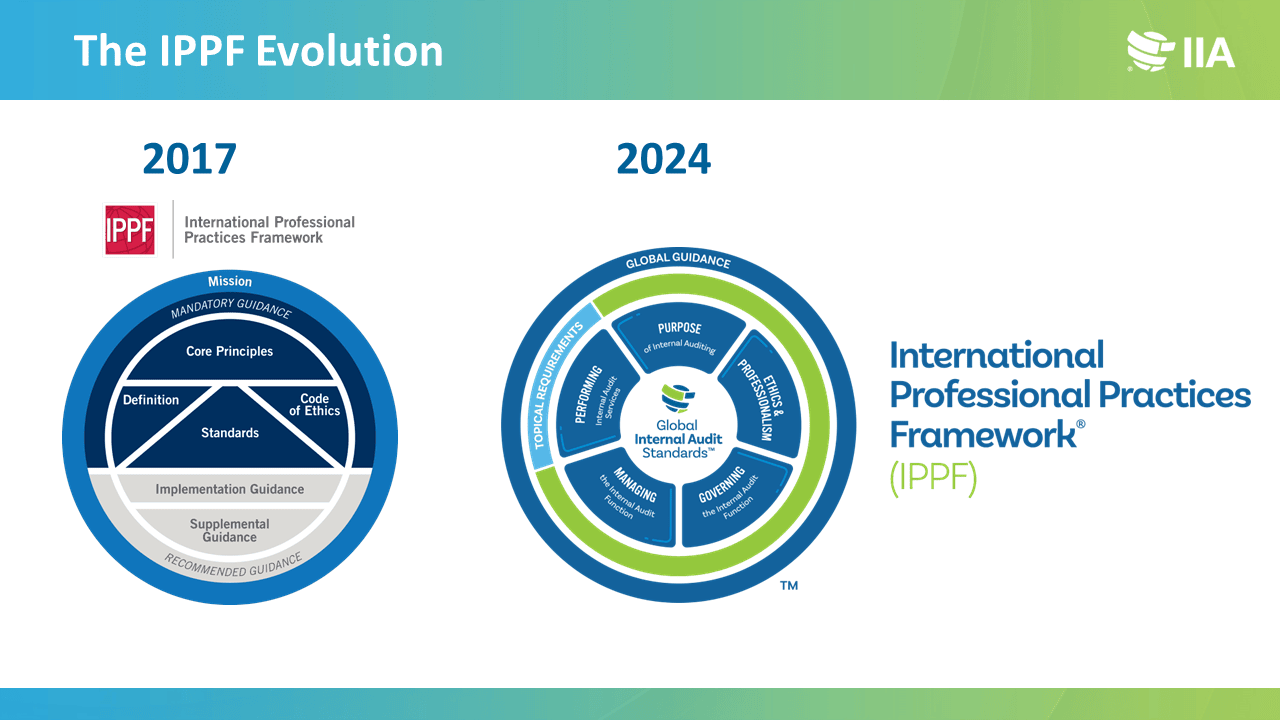

How Is The IPPF Changing?

The 2024 IPPF will include Global Internal Audit Standards, Topical Requirements, and Global Guidance.

- The Global Internal Audit Standards incorporate content from the five mandatory elements of the 2017 IPPF (Mission of Internal Audit, Definition of Internal Auditing, Core Principles for the Professional Practice of Internal Auditing, Code of Ethics, and Standards) as well as one of the recommended (nonmandatory) elements, the Implementation Guidance. These elements no longer exist as separate entities.

- Topical Requirements will be added as a mandatory element of the IPPF and aim to enhance the consistency and quality of internal audit services related to specific risk areas.

- Global Guidance will continue to be a recommended element in the new IPPF, providing in-depth information about various internal audit practices and subjects.

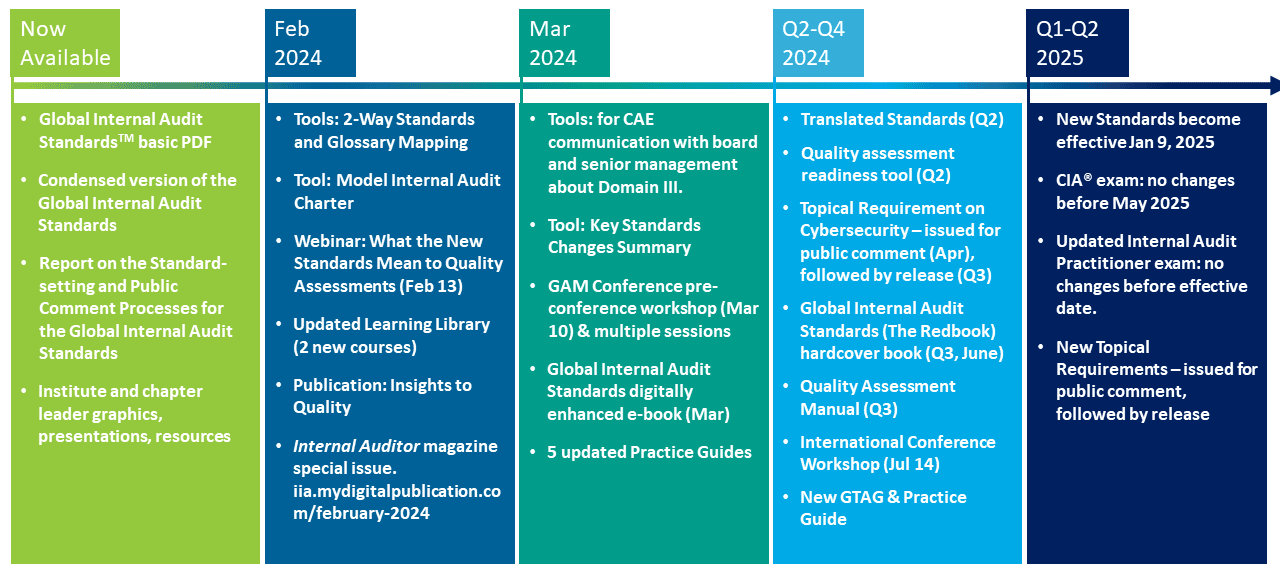

IPPF Evolution Timeline

Here is an overview of IPPF-related resources and when you can expect to see them.