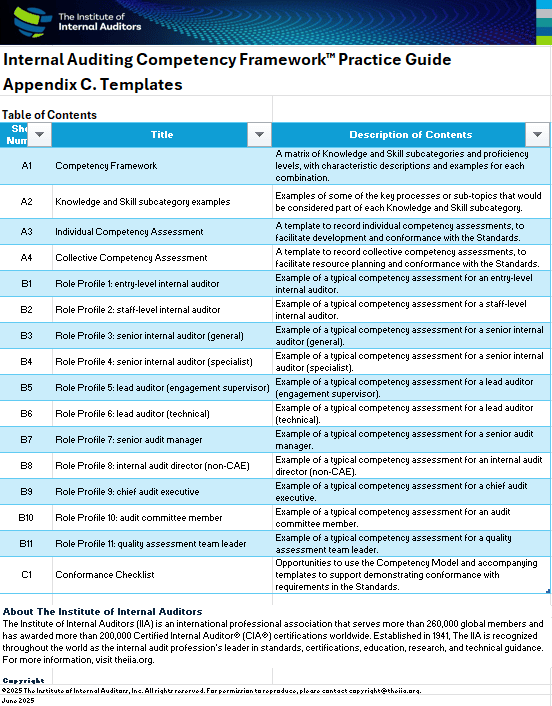

Tools

Internal Auditing Competency Framework Templates

Companion IIA Audit Tool of Global Practice Guide: Internal Auditing Competency Framework.